Patients deserve to know real prices and have a trusted, competitive marketplace for healthcare. Benefits advisor Carl Schuessler, Jr. describes how insurer-built plans have ceased to meet the needs of employers and employees, and how employer-built plans save costs for everyone by cutting out the middlemen. In this episode, you’ll learn what a fair cost health plan is, how it potentially improves business, and how real price transparency and direct contracting lower costs.

Engage With Us

How to listen: shows.pippa.io/paradigm-shift-of-healthcare/howto

Archive of previous episodes: https://www.p3practicemarketing.com/paradigm-shift-of-healthcare/

Follow on Twitter: https://twitter.com/p3practicemktg

Full Transcript

Announcer: It’s time to think differently about healthcare, but how do we keep up? The days of yesterday’s medicine are long gone, and we’re left trying to figure out where to go from here. With all the talk about politics and technology, it can be easy to forget that healthcare is still all about humans, and many of those humans have unbelievable stories to tell. Here, we leave the policy debates to the other guys and focus instead on the people and ideas that are changing the way we address our health. It’s time to navigate the new landscape of healthcare together and hear some amazing stories along the way. Ready for a breath of fresh air? It’s time for your paradigm shift.

Michael: Well, welcome to the Paradigm Shift of Healthcare, and thank you for listening. I’m Michael Roberts here today with my cohosts, Scott Zeitzer and Jared Johnson. On today’s episode, we’re talking with Carl Schuessler, Managing Principal with Mitigate Partners, a risk management, cost containment and employee benefits consulting group. Welcome Carl, thank you so much for coming on the show.

Carl: I appreciate the opportunity. It’s an honor to be on your show. I appreciate Dr. Kendrick Johnson introducing us and I’ve known Dr. Johnson for almost a year so that was really great to have a chance to be on the show. So thank you for the opportunity.

Michael: Oh, it’s our pleasure, sir. Our pleasure. So let’s jump right in. So you’re engaged in building employer billed health plans to replace insurer billed health plans. So let’s just start right back at the beginning. So how have insurer billed plans ceased to meet the needs of employers and their employees? And then I’ll go ahead and throw both questions in there so that we can kind of get your ready to go here. How do insurer plans then add to the cost burden for practices?

Carl: Sure. Well, first off, it’s a great question, Michael. Insurer billed plans have done nothing, but what they were supposed to do. The insurance company’s fiduciary responsibility is to the shareholders, the stockholders. So they have absolutely knocked the cover off the ball. As a matter of fact, any company that’s a publicly-traded company can take a lesson from the insurance companies because they have just delivered 20-fold on what they were supposed to. Problem is, as you said earlier, that comes to the cost and the detriment to the employer and also to their employees. So those programs are never geared to reduce costs because that’s the inverse opposite of what their stock price would be. Right?

So there’s misaligned incentives all over the place, so therefore the cost of the employer’s healthcare has done nothing but escalate and escalate and escalate. And the largest part of that is what we call the PPO escalator clause is that these insurance companies have and their network contracts with hospitals and physicians and so forth. So they are allowed four times a year to jack the prices. The hospitals are allowed four times a year to jack the prices, which the insurance company then gets a corresponding discount. So as the prices go up and the discount goes a little bit, the delta never closes. So we discovered that is a big problem. And plus there’s no transparency in that model whatsoever. And it’s set up, as I often say, healthcare isn’t broken, it was made this way. These people were geniuses.

Scott: Yeah, unfortunately, I think you’re absolutely right that they were geniuses. I kind of come back to this like fair cost plans. I think that’s central to what we’re talking about here and I wanted to get a little bit about what is a fair cost plan and how does it improve business for the practice itself and then ultimately I think for the patient too.

Carl: Right. Well, it’s a great question, Scott. Just to piggyback on the follow up question, and I’ll ask about employer built healthcare will falls into…

Scott: Yeah. I jumped on that. Yeah, you’re right.

Carl: It tails right into that. We decided seven years ago that that system wasn’t working. We were also part of the problem in the system. We were part of what I call the cartel, myself included and many other brokers at the time. We’re benefit advisors now is what we call ourselves. But we knew we couldn’t fix things. And the insurance companies using their models in the self-funded markets which is where we spend most of our time with large or medium to large self-funded employers, the insurer billed healthcare model didn’t work because it was the off the shelf solutions they had that they made money from. Anytime someone goes out of network, they get a percent of those savings. I mean, it goes on and on. It’s a litany of things. I could go on.

So we decided that we needed to make a change. That was also, we call it a passively managed health plan. So there was no active management whatsoever of it. So we knew that we needed to take control, deconstruct the entire system, rebuild it brick by brick, into what we call employer billed healthcare. And it’s truly customized for the employer and the employees or members of that company and therefore we’ve been able to improve clinical outcomes while improving financial outcomes for all parties. And so we designed what we call I guess it was over, like I said, a seven-year period, we brought together the best cost containment, risk mitigation solutions we could find across the world, and it did span across the world, and we seamlessly integrated them into16-plus solutions on this, what we call a fair cost health plan.

Scott: Okay. Walk me through that. Let’s make-believe… Well, first of all, let’s start with this. If you’re a company that’s medium to large size, what’s the smallest company that’s on your system right now?

Carl: Right now, it’s good question, Scott. We are developing a level-funded, if y’all are familiar with that, what that product level funded insurance. We’re developing a fair cost level-funded plan so that could go all the way down to 10, but the goal was to probably have it between 50 and 200. That’s a separate program we’re just in the process of developing because a lot of our mitigate partners were having groups between 50 and 100 employees and they didn’t have a lot of choices. They were using insurer billed level-funded plans. And we said, “What if you could take the fair cost self-funded plan and put it on a level-funded chassis?” And so that’s what we did. But on average, Scott, outside of that little piece that we’re working on, I would say, you know, 100 to 10,000.

Scott: Okay. So do you work with any larger companies, like Fortune 500 companies?

Carl: We do not. I’ve consulted with some companies, but I don’t believe any of them are Fortune 500 at this moment. Our biggest client is got about 10,000 belly buttons. It’s a school district.

Scott: Understood. So let’s kind of play with that one that just out of curiosity, like I’m kind of walking through this. So we’ve got this large group, whether it’s the school district or a smaller group. And to that point, like I’ve got 15 employees. So I’m definitely in that bucket where it’s like, I don’t know, “What am I allowed to buy and what can I then offer my employees?” But somebody who’s a little bit bigger, and that’s not that big, you know, 50 to 100 people. There are a lot of “small businesses” out there that are in that fold. What’s the difference? Like, what does a group like that get out of it? Walk me through that if you were gonna talk to me and I had say, 75 people in my team?

Carl: Seventy-five, I’d say, go fish, talk to somebody else.

Scott: Okay, 150. We’ll pull that number.

Carl: Well, we’ve got partners around the country that could help. For us, it’s the same amount of work for 75 as it is for a 1000. A lot of our business is probably honestly between 100 to 500. That’s a good, sweet spot. We can swim upstream any day of the week because it’s the same thing you’re doing there for that group, that size. But, so ask me that one more time, make sure I’m crystal clear.

Scott: Sure, man. Let’s make that number 500. Right? I got a decent-sized business gone. I got about 500 people. I’m kind of tired of the Blue Cross people coming in and going, “Here’s what you got.” You got your, what is it? Silver, gold, and whatever it is, plan, and you decide like, you know, for your business. Like in my business, I’ve basically made a choice that I try very hard to actually give everybody a maternity and paternity leave. We call it parental leave. I try to get more.

It still is boggles my mind that when you decide to have a baby, that it’s so costly, even if you are, I think we have the best plan in the State of Louisiana that’s where we’re based and still it costs my employees quite a bit of money to have a baby. So I come to you and I go, “Hey man, here’s some things that are important to me. I know you’ve got a lot of the details.” Walk me through like what I get from you and how it would work.

Carl: Great question. First off, I want to be crystal clear with you that the majority of our plants, not all of them, but the majority of them have no deductible.

Scott: Awesome.

Carl: So your members can actually go and take care of themselves without worrying. Today, we have what’s called, and I think Dave Chase has always said this, a functionally uninsured population. Yeah, they got insurance, but most people don’t have more than $500 in their checking account. So therefore, when they have a $3,000 deductible, they’re not getting the care they need or the drug copays are so high. So we usually have zero deductible. We have an out of pocket max Scott, but the chances of you hitting our out of pocket max, you have to take about 70 drugs a month to hit the out of pocket max. Okay? We have an admission copay. If they go, inpatient or outpatient, it’s very small. It could be $250 to $500. And then we have very innovative pharmacy or RX plan design where they can get generics usually for $0, many brand name medications for $0.

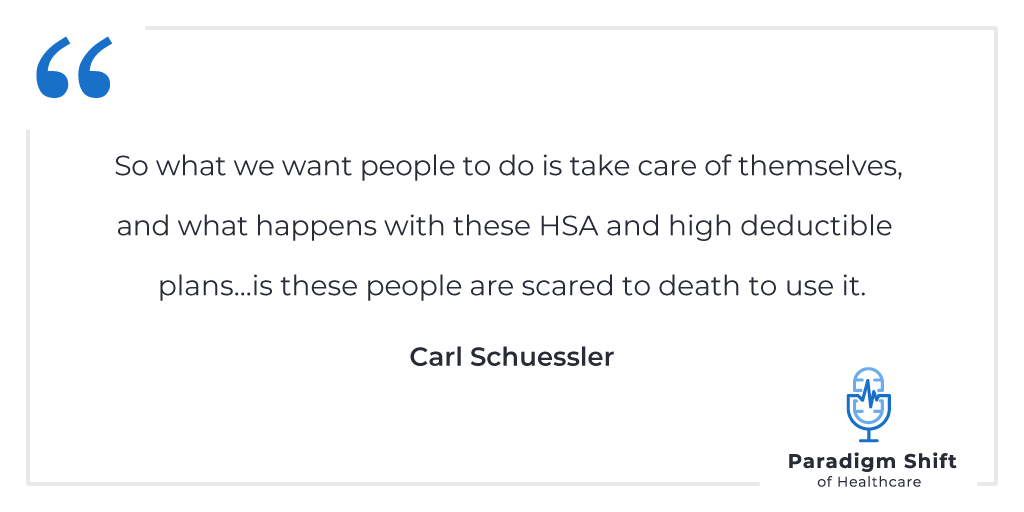

So what we want people to do is take care of themselves, and what happens with these HSA and high deductible plans that everyone’s buying for their employer, employees is these people are scared to death to use it. So therefore, they forgo meds and everything else. They don’t adhere to their meds. So we saw that as a problem and so, therefore, we changed that around making it totally accessible to members. And then we have all this cost containment and risk mitigation solutions to go along with this, Scott, behind the scenes that protect the employer from potential things happening in the health plan, but also like we said, encourage the employee to use the plan. And that’s those 16 solutions, many of them behind the scenes. And we can talk about our cost and quality solution if you want to in a minute, how we do those things. But does that answer your question?

Scott: Yeah, I think it does. And it kind of lends me, like I was just thinking about while you were talking to me about price transparency which is a big part of the news right now with the Supreme Court decision that just came out, etc. And is that a big part of what you get down to like health, in terms of, do you negotiate for the company via transparency where it might be better for, you know, a local person to go get a, I’ll just make something up, a CAT scan. A CAT scan at one place is going to be…and believe me, I’ve tried. I remember I had a family member who needed to get an MRI for a bad knee, ended up needing to get scoped, and it was just amazing about how difficult it was to just simply say, “Hey, what’s it cost to get a scan of my knee?” It was ridiculous. I don’t know.

Carl: I want to address one thing you said in that quote, in that very filled question. I think it’s real important if we look at the system we work in today. Scott, I got a car for you today and I want you to take it off my hands. You’re in need of a car, just take it. And you ask me how much and I say, “Don’t worry about it, Scott. Just take the car.” “How much is it Carl?” Just take the car. Thirty days later, you get a bill from me for $100,000 and you pick the phone up and say, “Carl, what in the heck is this bill for $100,000?” “Well, that’s the cost of the car you took.” “Well, I asked you how much it was and I asked you all these questions you didn’t tell me.” So where else in America do we go and use and purchase services without knowing the cost for 30 days? And again, what do we say? Healthcare isn’t broken, it was made this way. Brilliant, and it continues.

So in our plan, what we did is we have a cost and quality company led by nurse navigators, overseen by an MD. And you are required in our plan, Scott, to call for any elective or pre-certed procedure such as a CT scan would be a pre-certed or elective procedure, and you’re required to call. If you do not call, some of our clients impose penalties. If you do not call, then you’ll be penalized $1000. If you call, the penalty’s off, and then you have two choices. Listen to the nurse navigator and they say, “Go see Schuessler Imaging over here, the best quality image in the entire country at a quarter of the cost,” or Scott, because you’re difficult and you’d like, it’s a free country and you want to go where you want to go because you don’t want to listen, you go over here to Johnson Imaging and it’s X. If you go to Schuessler Imaging where they told you to go, then maybe if you had a deductible, remember we don’t have them, then your co-pays are waived. There’s no cost to you to go over there. Or if you want to follow and go to Johnson Imaging and do your own thing, then there might be a cost associated with that.

So the member always has a choice in our program. Normally they have three choices. And some clients don’t impose penalties. And here’s one thing I can tell you. When you don’t impose a penalty, you put your plan at risk and that member, it’s really difficult to make that member call that nurse navigation company. The biggest part, Scott, this isn’t Big Brother looking after you. This is finding out what the best care for you is. My father was a 40 year OB-GYN in private practice in Macon, Georgia. I know you thought I was from New York City, but I’m really not. He practiced for 40 years. And I remember working at the golf course in the summers and I had a job there and I’d say, “Hey pop, why are you never at the golf course? Dr. Stalls is always at the golf course.” Well son,” and he’s a solo practitioner OB-GYN.

My dad had three partners at that time. And he goes, “Son, his C-section rates are over 50%. Mine’s 15%.” Now, I don’t know about you, but my wife, Missy, I’d like to know that Dr. Johnson is gonna cut my wife open 50% of the time versus 15%. That’s the information that you can’t find in the system anywhere because it’s not published. You have to have a company to help you do it. That’s the kind of thing. So we looked at readmit rates, complications, you know, those types of things and almost always price is the inverse opposite of quality in healthcare. The more expensive something is in healthcare, the quality is usually worse. Because, you want to know that Dr. Schuessler does 500 deliveries a month before you go to them, don’t you? That’s the things you can find out. And I hope that helps. Does that help?

Scott: It really does. It really does.

Jared: I really feel like, Carl, this part of the conversation is so fascinating because I feel like two things that you said. I mean, first and foremost, how there are benefits for the employer to figure all this out. Is that gonna offer their benefits to the employees, because the one thing you said is how you want employees to take care of themselves, take better care of themselves at the end of the day? I mean, you talk about misaligned incentives, and that is the story of this entire side of what’s going on with paying for health care. So I wonder if we could dive into a little bit more the part about how the right type of health plan really does encourage an employee to be healthier. I mean, just like kind of a basic level. Right? That’s the part for the employee that they’re maybe not factoring in at all, either. How does the right type of health plan if it’s structured right help them take care of themselves better?

Carl: Great question, Jared. Again, if you have no deductible and low copays, you’re encouraging people to take care of themselves. If you have a diabetic, for example, we’re charging, these health plans across America are charging for these test strips for their A1C and all the diabetic supplies. A lot of these people can’t afford them, so they’re not taking them. Right? So what we’ve tried to do is if the employee will see that, and we’re big on community pharmacists, we’re big on re-localizing care, keeping the dollars local. Healthcare is local, not national. So we’re not big on using the cartel pharmacy chains.

If I need to call those out, I can to you, but I might be careful because I don’t want my car to blow up today. But anyway, long story short, if you see the community pharmacist that we picked and you meet with them once a month for 15 minutes on your diabetic education, they can synchronize your meds for you so you walk out with a bag of your meds and you can adhere to your meds, which means you don’t end up in an ER, you don’t end up in an inpatient admit, et cetera. So we’ve got to make these medications affordable for the people so they adhere to them.

I was on a high deductible HSA plan. My family, I got family of five counting myself, and I was taking Vytorin for cholesterol, and it was $300 a month. I could afford that, but it irritated me. So I quit taking it. You think Johnny Lunchbucket is going to be able to take a $300 a month medication? No, he’s just not going to take it. Then he ends up with a heart attack down the road and blows your health plan up. So we want to make the meds at a good price for everybody so they can afford to take them and adhere. We want to make them go get their checkups and we can incentivize them to do that. We want to break all barriers to care. That’s what’s important. The system is set up for sick care right now.

That’s what’s wrong with it, and I think COVID-19 pointed out bigger than ever, the need for direct primary care if you’re all familiar with DPC. We need those kind of doctors to sit and diagnose and meet with patients, have a real relationship with them, not with some EMR system they’re typing on while you’re trying to talk to them, but a relationship with them so they can take care of them and they can spend 30 minutes to an hour with them.

They can get them off opioids like we’ve seen Dr. Lee Gross do down in Arcadia, Florida with our hospital client, DeSoto Memorial Hospital. Dr. Gross is a fantastic physician who has done a ton nationally for DPC and also for his own State of Florida. So that’s what we have to get back to. We need a patient-doctor relationship and what I call the local care team, the pharmacist, the primary care doctor, the specialist, and the member, the employee. And I call it the love triangle. As perverse as that sounds, that’s what has to happen. And right now the middle people, the insurance companies and the PBMs, program bilking millions, are all interfering in the care of that individual. Back in the days of Marcus Welby M.D. as I’ll often say all the time. Marcus Welby M.D. took care of people.

There was nobody telling him what to do. People saw him because it was their choice. My mother in the late ‘80s, getting ready to go off to the Harvard of the South, University of Georgia, I had to get my… That’s not funny guys. I had to get my physical done and I remember going into the doctor’s office at that time. And it was Miss Yancy, a little fireball of a nurse practitioner and she scared me to death. And I knew that she was going to want to draw my blood, but it was gonna be that finger prick back in the day when they didn’t have the hole punch.

Today everybody gets off easy. It was that razorblade and you had gauze pad for like an hour after it was done. I hated that. And I knew that was coming. I was sweating bullets. It was August, 1985, it was hot as fire in Macon, Georgia. One of the hottest place on earth, by the way. And also I’m in that room in this old antebellum home, all freaked out sweating. And I looked around the room. How many people do you think were sitting at room August 1985 in the waiting room? Anybody?

Scott: I’m gonna guess six people.

Carl: Zero. Okay. Do you know why?

Scott: Just close to my six.

Carl: Do you know why? I know you’re going to say, “Carl, aren’t you in your 50s? You’ve probably already seen I don’t have dementia. How can you remember that?” There was nobody in there because that was a healthcare visit. My parents paid out of their pocket for it. There was no insurance involvement whatsoever. And that’s when, late ‘80s and early ‘90s in the South where I’m from, that’s when managed care rode and came in. I’ll never forget it. My mother had a sticker on her car, “My doctor, my choice.” Now, if you didn’t grow up with some of these issues, you can’t really appreciate that. But watching what happened to my father, watching people tell him how to practice that knew nothing about medicine and watching a patient, Scott’s wife came to my dad for 20 years, and he decided, “I’m not doing this network stuff. We’re not gonna do it in our practice.”

And all of a sudden Scott’s wife came in and said, “Dr. Schuessler, you have been great. I really appreciate these last 20 years, but you’re not in my network, can’t come anymore.” My dad was floored and he knew then, it’s over. That was the prediction and he was dead on as he often was growing up. Unfortunately, he was right too much. But anyway, that’s my story on that. We need good primary care and that’s what COVID-19 is pointing out more than ever.

Scott: Yeah. We’re coming up on the end and so a couple of thoughts here. One, as far as I know, Tulane, where I went to school is Harvard of the South. Nothing against the University of Georgia, but that’s for another…

Carl: Whatever.

Scott: We could have some fun with that. But yeah, I really do. We’ve had quite a few podcasts and if you are listening to some of our podcasts where we’ve talked to a lot of different primary care providers and how they have come up with a way to avoid, “The system” so that they could actually just take the time to take care of their patients, to get to know their patients, and like you said, not to get to know their EMR and how quickly they can enter data in.

I’ll leave people with this story. I had a primary care provider that I knew very well. He was much older than me and he retired and I had to go get another primary care provider and I ended up at a…basically it was a, from, I didn’t know this, I was just another primary care provider. I don’t want to give away the name or anything, but they took my weight. I was wearing a suit and I was carrying my laptop back. And they took my weight, walked in and then someone started taking my history, which I had already taken the time to write down. And I said, “Is there a reason why you’re asking me these questions over that I’ve already written down for you?” And they said, “Well, you know, I have to.” And I said, “Okay. Are you a registered nurse?” “No.” And she was about to take my blood pressure, which I’m guessing at that point was going higher and higher.

And I said, “Well, you know, what medical qualifications do you have before you start taking my blood pressure?” And she said, “I have not.” And I said, “Well, then why don’t we take a pause and I’ll go and meet with the doc.” And he came in and he said, well, my BMI looks good. And I said, “Was that with the computer or without the computer?” And he had no idea. And he goes, “Well, you’re doing okay, man so I wouldn’t worry too much.” And I said, “Look, man, if you want to bill me, bill me, but I’m gonna be going to my insurance company and saying, ‘Please don’t bill me for this visit.’ You don’t deserve the money.” It does center around this, doesn’t it? My perspective is like, we gotta get back to let doctors take care of their patients. They actually like taking care of their patients.

Carl: It’s what they train for. Doctors get beat up a lot on many things and, you know, only thing I ever told my father while they sat there and watched all these business executives in managed care take their practices away because they were taking care of patients. That’s what they were trained to do. They weren’t trained to do all that lobbying and stuff. I think agree with you 100%. Dr. Kendrick Johnson is great. I love what he’s doing out there in Phoenix. And I know telehealth has gone off the hook over there and for everyone of these people and of course, across the country. Isn’t that interesting, Scott and Jared, how different, how now telehealth is like unbelievable because that’s all people have or are comfortable with it right now. So I think that that revolution is important.

And I think one thing too, I want to say just this, I know we didn’t get into the videos, with the client videos for patient rights advocate, but I think the work that they’re doing, I seen the official one with James and Carey, Alaria Santiago, and they’re doing such wonderful work and I’m leaving a lot off. But I want to say one thing that one of our Mitigate Partners advisers, Cristy Gupton says, and there was a show they did a couple of weeks ago where they took this and ran with it. But all it takes is a good advisor and a little courage. And advisors, there’s a group of us in the health, Rosetta, over 200 and there are other good advisors as well, but there’s also a lot of brokers who were part of the cartel and part of the problem. It’s the easy button, like we said, the passively managed plan is easy. It’s easy button. But employer billed healthcare, you got a want it because it’s not easy, but the fair cost health plan makes it easier and you can actively manage risks. But Cristy said it takes a good advisor and a little courage.

And the courage is on us guys. The courage is the employer. It takes the courageous employer, the hospital, the hotel, the school district that will step out and follow our advice, but we have to make them courageous, make it where they’re not left out there blowing in the wind in trouble, you know, because they made a bad decision. That is what’s critical. That courageous employer. And I can’t thank our clients enough for being courageous and having these great stories to share with the rest of the country. And we have to share and collectively we can fix it. There’s never been a better opportunity to be a benefits advisor right now. And there’s never, I don’t think a more important occupation right now, as Dave Chase said a few years ago, than a benefits advisor because we can change this one employer at a time.

I tried to boil the ocean in DC, that didn’t turn out too well for me. So we have to boil the creeks, boil the rivers, boil the lakes, and then we get to the ocean. That’s how we have to do it and that’s what our Mitigate Partners with coupled with the fair cost health plan and also the health advisors around the country, that’s what we’re trying to do.

Michael: Awesome. Well, Carl, it’s been such a pleasure to speak with you. Thanks for opening up this world to us and giving us a little glimpse of the revolution that’s happening behind the scenes and given us some reason for hope genuinely. I mean, we just wish you all the best. Wish you stay safe and stay well and keep up this great work. We can’t wait to hear more.

Carl: I appreciate the opportunity and I thank you so much for your time and helping folks like you guys with these great podcasts for helping this move faster and hopefully saving this malfunctioning and as I call it archaic healthcare system. So thank you, guys.

Scott: All good. All good. Have a great day. Everybody stay safe. Stay well.

Carl: All right, thanks.

Announcer: Thanks again for tuning in to “The Paradigm Shift of Healthcare.” This program is brought to you by P3 Inbound, marketing for ortho, spine, and neuro practices. Subscribe on iTunes, Google Play, or anywhere you listen to podcasts.

P3 Practice Marketing has helped orthopedic, spine, and neurosurgery practices market themselves online since 1998. Our focus is on helping practices expand their reach through increased patient recommendations and provider referrals.